Why Book Value Is a Dangerous Comfort

A Data-Driven Analysis of Where This Metric Works, Fails, and Actively Misleads Investors

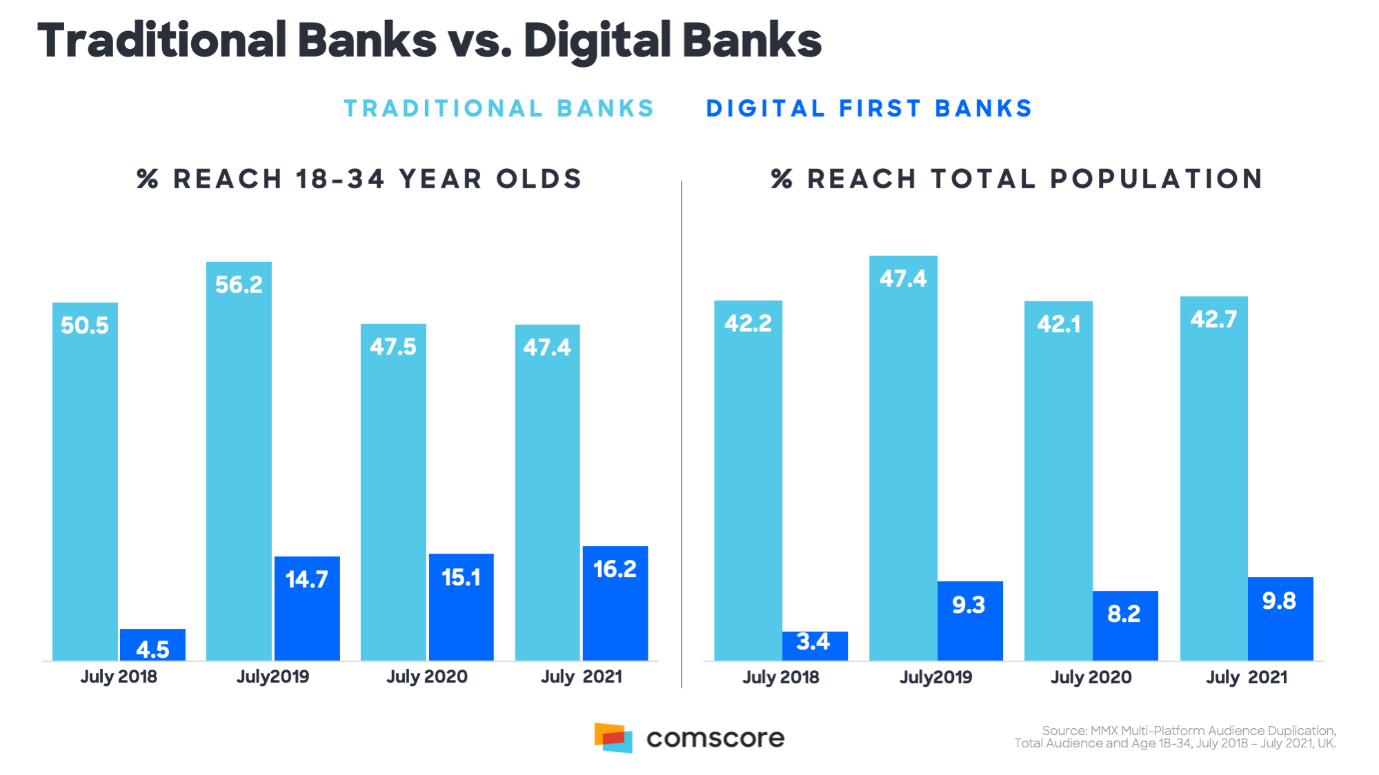

Dividend yield often feels comforting, but total return tells the real story.

The Fundamental Illusion: What Book Value Actually Is

At its core, Book Value is an accounting construct: Total Assets minus Total Liabilities. It answers a theoretical question: "If the company liquidated today at the values on its balance sheet, what would be left for shareholders?"[citation:3]

function calculateBookValue(totalAssets, totalLiabilities) {

return totalAssets - totalLiabilities;

}

// And the derivative, Price-to-Book (P/B) Ratio

function calculatePriceToBook(marketPricePerShare, bookValuePerShare) {

return marketPricePerShare / bookValuePerShare;

}

The critical flaw is in the phrase "values on its balance sheet." These are historical costs, often smoothed by depreciation, and they frequently ignore intangible value and economic reality[citation:8]. A brand's power, a software platform's network effects, or a pharmaceutical company's research pipeline rarely find accurate representation in book value.

⚠️ The Core Misunderstanding: Investors often treat a low P/B ratio as a "margin of safety." However, if the assets on the balance sheet are overvalued, obsolete, or generate poor returns, that margin is pure fiction. The safety lies in the business's economics, not its accounting.

The Statistical Mirage: Why P/B vs. ROE Charts Can Deceive

A common analytical technique is plotting a company's Return on Equity (ROE) against its P/B ratio. The apparent correlation seems to validate the metric—higher returns justify higher valuations relative to book value. However, this relationship can be mathematically misleading[citation:6].

// P/B = Price / Book

// ROE = Earnings / Book

// Therefore, P/B divided by ROE = (Price/Book) / (Earnings/Book) = Price/Earnings

function revealTruePERatio(priceToBook, returnOnEquity) {

return priceToBook / returnOnEquity; // This is the Price-to-Earnings (P/E) ratio

}

// Example: A stock with P/B of 2.0 and ROE of 15%

let pe = revealTruePERatio(2.0, 0.15);

console.log(`The underlying P/E ratio is: ${pe.toFixed(1)}x`); // Output: 13.3x

This code reveals a crucial insight: A P/B versus ROE chart is often just a disguised P/E ratio analysis[citation:6]. The correlation is frequently driven by similarities in P/E ratios across a sector, not by book value being a superior measure. You can even generate seemingly strong correlations using random numbers for book value, which highlights the statistical fragility of the relationship[citation:6].

Where Book Value (Sometimes) Works: The Asset-Heavy World

Book Value has meaningful relevance in industries where balance sheet assets are core to operations and have a clear market value.

Banks & Financials

Assets (loans, securities) and liabilities (deposits) are financial, marked-to-market, and heavily regulated. P/B is a key capital adequacy metric.

Insurance Companies

Massive investment portfolios and actuarial liabilities make the balance sheet central to the business model and solvency.

Capital-Intensive Industrials

For utilities, steel, or cement, the replacement cost of plants and machinery is a relevant economic benchmark, though earnings power is still paramount[citation:8].

The chasm between asset-heavy and asset-light businesses makes a single valuation metric like P/B ineffective.

Where Book Value Utterly Fails: The Modern Economy

In today's market, value is increasingly derived from intangible assets and competitive advantages that accounting rules poorly capture.

| Business Type | Source of Value | Why Book Value Fails |

|---|---|---|

| Technology & Software | Platform networks, code, user data, brand | R&D is expensed, not capitalized. The primary assets (intellectual property, talent) are off-balance-sheet. |

| Consumer Brands (FMCG) | Brand equity, distribution, customer loyalty | A global brand like Coca-Cola is worth billions but appears as a minor intangible asset. |

| High-ROE Compounders | Exceptional capital allocation, scale, moats | Their value is in the future cash flows they can generate from retained earnings, not past capital invested. |

💡 Key Insight: A company trading at a high P/B multiple isn't necessarily "expensive." It may simply be an enterprise whose value-generating assets are invisible to the accountant's ledger. Conversely, a low P/B company might be a "value trap" where the reported assets are economically impaired or generate subpar returns.

A Better Framework: Moving Beyond the Balance Sheet

To avoid the book value trap, shift your analysis from accounting aggregates to economic drivers.

class EconomicValueAnalyzer {

constructor(company) {

this.company = company;

}

// Focus on the return, not just the base

assessQualityOfReturns(roe, trend, industryAvg) {

let score = 0;

if (roe > industryAvg * 1.5) score += 2; // Superior returns

if (trend === 'stable' || trend === 'improving') score += 2; // Sustainable

return score >= 3 ? "High-Quality Returns" : "Investigate Further";

}

// Check if the business model is asset-light

isAssetLightBusiness(capexToRevenue, intangiblesImportance) {

return capexToRevenue < 0.05 && intangiblesImportance === 'high';

// If true, book value is nearly irrelevant for valuation.

}

}

The Psychological Trap: Why We Cling to Book Value

The appeal is behavioral. Book value feels tangible, conservative, and quantifiable. It satisfies a deep need for an "anchor" in the chaotic market, similar to how a high dividend yield can feel like a tangible reward[citation:4]. This psychological comfort often overrides more nuanced, forward-looking analysis of a business's cash flow generation and competitive moat[citation:3].

Investment decisions are a battle between psychological comfort and economic reality.

Practical Checklist: When to Use (and Ignore) Book Value

Use Book Value/P/B as a primary tool only when:

- Analyzing financial institutions (banks, insurance).

- Assessing deeply cyclical, asset-heavy firms where replacement cost matters[citation:8].

- Screening for potential bankruptcy or liquidation scenarios (where liquidation value is key).

Downgrade or ignore Book Value when:

- Evaluating technology, software, or consumer brand companies.

- Analyzing any business with high and sustainable ROE driven by intangible advantages.

- The business model is explicitly asset-light.

The most successful investors understand the context behind every metric. They don't ask, "Is the P/B low?" They ask, **"What is the economic nature of this business, and does this accounting metric help me understand its intrinsic value?"** That shift in questioning is the difference between falling for a trap and finding genuine opportunity.

{kind=link}