Wealth isn’t built by choosing the hottest fund category; it’s built by choosing an allocation you can hold through panic

Most investors think this is a “basic” question.

Large cap = safe. Mid cap = moderate. Small cap = risky.

That’s the oversimplified version.

And oversimplified thinking is exactly why portfolios collapse during market crashes.

If you want to build serious wealth through mutual funds, you must understand not just the definitions — but the behavior, psychology, volatility patterns, and long-term return dynamics of each category.

Let’s break it down properly.

First: What Does “Cap” Even Mean?

“Cap” stands for market capitalization.

Market capitalization = Share price × Total number of outstanding shares.

It represents the size of a company in the stock market.

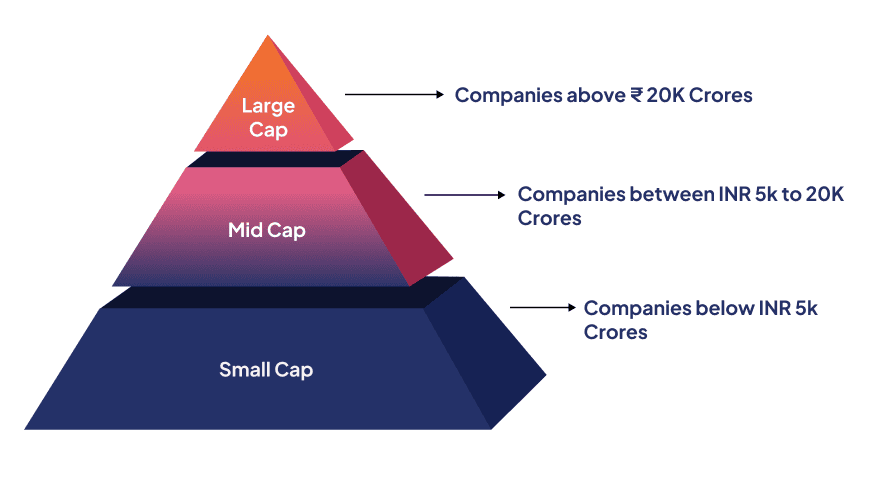

In India, companies are categorized (as per SEBI classification framework) broadly into:

- Large Cap (Top 100 companies by market cap)

- Mid Cap (101–250)

- Small Cap (251 and beyond)

Mutual funds that primarily invest in these categories are called large cap, mid cap, and small cap funds.

Now the real conversation begins.

Large Cap Funds – The Stability Engine

Large cap funds invest in established companies — industry leaders. Think of giants like:

- Reliance Industries

- Tata Consultancy Services

- HDFC Bank

- Infosys

These companies have strong balance sheets, established market presence, stable earnings, and institutional investor confidence.

What Happens During a Market Crash?

Large caps fall. But they usually fall less compared to mid and small caps. And they recover faster. Why? Because institutions, FIIs, and large domestic funds prefer parking money in established businesses during uncertainty.

✓ Pros of Large Cap Funds

- Lower volatility

- More predictable earnings

- Better liquidity

- Stronger downside protection

✗ Cons of Large Cap Funds

- Slower growth potential

- Lower explosive upside

- May underperform in strong bull markets

If you're expecting 40% annual returns from large cap funds consistently, you're either uninformed or unrealistic.

Mid Cap Funds – The Growth Accelerator

Mid cap companies are not small, but not giants either. They are in expansion phase. They’ve proven their model — but are still growing aggressively. Mid cap funds invest in companies ranked roughly 101–250 by market capitalization.

These companies often expand market share, enter new regions, innovate aggressively, scale revenue faster than large caps.

Behavior During Market Cycles

In bull markets: mid caps often outperform large caps. In bear markets: they fall harder. Why? Because growth expectations shrink quickly during economic uncertainty. Mid caps are more sensitive to interest rate changes, liquidity tightening, economic slowdowns.

✓ Pros of Mid Cap Funds

- Higher growth potential

- Better return opportunity over long term

- Ideal for wealth creation phase

✗ Cons of Mid Cap Funds

- Higher volatility

- Deeper drawdowns during crashes

- Requires longer holding period

If you panic during a 25–30% correction, mid caps will test your emotional stability.

Small Cap Funds – The Volatility Beast

Small cap funds invest in companies ranked 251 and beyond. These companies have high growth potential, are less researched, have limited liquidity, and may have weaker financial buffers. Small caps can multiply money dramatically in strong economic cycles. They can also crash 40–60% during downturns. Yes. 50% drawdown is possible. And many investors underestimate this.

Why Small Caps Swing Wildly

- Lower institutional participation

- Lower liquidity

- Higher business risk

- Speculative inflows during bull runs

Small caps are not bad. They are simply volatile. Volatility is not risk if you understand time horizon. But it becomes risk if you lack discipline.

The Real Difference Is Not Size – It’s Behavior

Let’s simplify the behavioral pattern.

| Category | Growth Speed | Volatility | Crash Impact | Recovery Speed |

|---|---|---|---|---|

| Large Cap | Moderate | Low | Lower | Faster |

| Mid Cap | High | Medium-High | Deeper | Moderate |

| Small Cap | Very High | Very High | Severe | Slower, uneven |

Now ask yourself: Can you emotionally handle a 40% portfolio decline? If not, loading small cap funds is self-sabotage.

Return Expectations – Let’s Be Realistic

Over long time horizons (10+ years): Large Cap → stable wealth compounding; Mid Cap → strong wealth building; Small Cap → high return potential with extreme cycles. But here’s what most beginners misunderstand: small caps do not outperform every year. They go through long underperformance phases. If you enter at peak euphoria, your returns may stay flat for years. Patience is non-negotiable.

Time Horizon Changes Everything

Your age and goals matter more than fund category.

If You’re 25–35 you can take higher exposure to mid and small caps. Time absorbs volatility.

If You’re 35–45 balanced allocation becomes smarter. Combination of large + mid + some small.

If You’re Near Retirement heavy small cap exposure is dangerous. Capital preservation matters more than aggressive growth.

Portfolio Allocation Strategy

Here’s a disciplined approach:

- Conservative Investor: 70% Large Cap, 20% Mid Cap, 10% Small Cap

- Moderate Investor: 50% Large Cap, 30% Mid Cap, 20% Small Cap

- Aggressive Investor: 30% Large Cap, 40% Mid Cap, 30% Small Cap

But don’t copy this blindly. Allocation depends on risk tolerance, income stability, emergency fund strength, investment horizon. If you don’t have 6–9 months emergency fund, aggressive allocation is irresponsible.

Common Mistakes Investors Make

Mistake 1: Chasing Past Returns – Investing in small cap funds after they already delivered 50% returns. Late entry = regret.

Mistake 2: Ignoring Valuation Cycles – Even good companies become bad investments at high valuations.

Mistake 3: No Rebalancing – If small caps grow rapidly, your allocation becomes skewed. Rebalancing protects gains.

Mistake 4: Panic Selling During Crash – Small caps fall 40% → investor exits → recovery missed. Emotional discipline > market timing.

SIP Strategy Across Market Caps

SIP works differently across categories.

Large Cap SIP: smooth returns, lower volatility, predictable compounding.

Mid Cap SIP: higher NAV fluctuation, strong long-term potential.

Small Cap SIP: very volatile, requires patience, best suited for long-term investors (10+ years).

Stopping SIP during downturn destroys rupee cost averaging benefit. Consistency builds wealth.

Market Cycle Awareness

When economy is strong: small caps outperform, mid caps shine, large caps may lag.

When uncertainty rises: large caps outperform, mid caps struggle, small caps crash.

Smart investors diversify across cycles. Not bet everything on one phase.

Should You Choose One or Combine?

If you're beginner: start with large cap or flexi-cap.

If you're intermediate: add mid cap exposure.

If you're experienced and disciplined: add controlled small cap allocation.

Concentration increases risk. Diversification increases survival. And survival is the first rule of investing.

The Psychological Reality

Large caps test patience. Mid caps test conviction. Small caps test emotional stability.

Most investors think they are aggressive. Until their portfolio drops 35%. Risk tolerance is revealed in red markets, not green ones.

Large cap vs mid cap vs small cap is not about which is “best.” It’s about where you are in life, how strong your income is, how disciplined you are, how long you can stay invested, whether you panic easily.

The middle class often makes one big mistake: they want small cap returns with large cap stability. That combination does not exist. If you want high growth, accept volatility. If you want stability, accept moderate returns.

Wealth is not built by chasing categories. It is built by clear allocation, long-term discipline, emotional control, strategic rebalancing.

Now let me challenge you. Are you writing this blog just to explain differences? Or are you building a structured mutual fund education series? If you’re serious, your next articles should logically connect: “How to Build a Diversified Mutual Fund Portfolio”, “SIP Strategy for Different Risk Profiles”, “How to Rebalance Your Portfolio Annually”. Pick a direction. And build depth. What is your long-term goal with this blog — traffic, authority, affiliate income, or positioning yourself as a finance expert?

— You can’t demand small-cap returns while expecting large-cap stability — every reward in the market comes with a price called volatility —

{kind=link}