Smart investors chase returns. Wealth builders design structures — and a HUF is where tax planning turns into long-term power.

Introduction: Most People Ignore This Legal Tax Tool

If you’re serious about building wealth in India, you cannot afford to ignore the structure that the law already gives you: the Hindu Undivided Family (HUF).

While many investors obsess over stock picks, SIP returns, and “multibagger” ideas, they completely ignore tax structure. That’s a mistake. Because smart structuring often saves more money than smart investing.

A HUF is a separate legal and tax entity under Indian law. And when used correctly, it can legally reduce tax liability on investments, rental income, business profits, and capital gains.

This is not a loophole. This is not evasion. This is structured wealth planning.

Let’s break it down step by step — clearly, practically, and strategically.

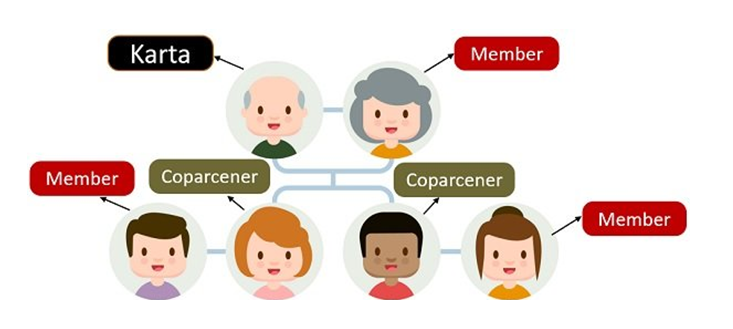

What is a HUF?

A Hindu Undivided Family (HUF) is a family unit recognized under Indian tax law. It consists of:

- A Karta (head of the family)

- Coparceners (members with birthright in ancestral property)

- Other family members

It is governed by Hindu law and recognized under the Income Tax Act, 1961.

Key point: 👉 A HUF is treated as a separate taxpayer.

That means:

- It gets its own PAN

- It files its own income tax return

- It enjoys a separate basic exemption limit

- It can claim separate deductions

If you ignore this structure, you are voluntarily paying more tax than required.

Who Can Form a HUF?

A HUF can be formed by:

- Hindus

- Sikhs

- Jains

- Buddhists

The moment a Hindu family exists, a HUF technically exists. But for tax purposes, you activate it formally by:

- Creating a HUF deed

- Applying for a separate PAN

- Opening a bank account in the HUF name

Simple. Legal. Structured.

Why HUF is Powerful for Investors

Here’s the strategic thinking most people miss:

If your income is high, your tax slab is high. If your tax slab is high, investment returns get taxed harder.

Now imagine shifting part of your investments into a separate tax entity that has:

- Its own ₹2.5 lakh basic exemption

- Separate deductions under 80C

- Separate capital gains taxation

That’s leverage. This is not about “saving a few thousand.” This is about building long-term compounding with lower tax friction.

Core Tax Benefits of HUF

1. Separate Basic Exemption Limit

Just like an individual, a HUF gets ₹2.5 lakh basic exemption (under old regime). So if your HUF earns ₹2.5 lakh annually from investments, that income can effectively be tax-free.

Most people let all investments sit in their personal name and pay higher slab rates unnecessarily.

2. Separate 80C Deduction

HUF can claim up to ₹1.5 lakh under Section 80C independently. That means: if you invest ₹1.5 lakh personally and another ₹1.5 lakh through HUF, you effectively double the deduction.

Eligible instruments include:

- ELSS mutual funds

- Life insurance premium (for members)

- PPF (in some cases)

- Tax-saving FDs

3. Tax on Capital Gains

HUF can invest in equity shares, mutual funds, bonds, real estate. Capital gains taxed at same rates as individuals. But if HUF has low overall income, gains may fall into lower brackets. Especially powerful when the Karta is already in 30% slab.

4. Income Splitting Strategy

If you earn ₹25 lakh (30% slab) and invest personally, all interest/dividend gets taxed at 30%. But if capital is transferred properly to HUF, investment income is taxed in HUF’s slab — often at lower rates. Legal income distribution. Lower effective tax. Not evasion. Allocation.

Example: Real Tax Saving Scenario

Let’s assume: Mr. Sharma earns ₹20 lakh per year (30% slab). He has ₹10 lakh surplus to invest.

Scenario 1: Invest Personally

Returns at 10% = ₹1,00,000

Tax at 30% = ₹30,000

Net = ₹70,000

Scenario 2: Invest via HUF

HUF earns ₹1,00,000

If within exemption → Zero tax

Net = ₹1,00,000

Difference: ₹30,000 per year. Now multiply that over 15 years with compounding. That’s serious money.

Where HUF Works Best

1. Rental Income from Property

If ancestral property generates rental income: tax can be paid by HUF instead of individual, deduction under Section 24 available, structured asset holding possible.

2. Equity & Mutual Fund Investments

HUF can open Demat account, invest in stocks, mutual funds. Ideal for long-term family wealth, SIP-based investing, dividend-yield portfolios.

3. Family Business Income

If a small family business exists: profits can be earned in HUF name. Salary paid to Karta is allowed (deductible expense). Advanced structuring — but powerful when done correctly.

Funding a HUF: The Right Way

Now pay attention — this is where people make mistakes. You cannot randomly move your salary into HUF and avoid tax. There are rules.

Sources of HUF funds can include:

- Ancestral property

- Gifts from relatives

- Gifts received at marriage

- Assets transferred under will

- Capital introduced at formation

Clubbing provisions apply if you transfer personal assets without proper planning. So don’t do half-knowledge tax structuring. Consult a CA before major transfers.

Limitations of HUF (Be Realistic)

- Partition is complicated – dissolving HUF requires legal process.

- All Coparceners have rights – you don’t have unilateral control forever.

- Increasing scrutiny – improper structuring can invite tax notices.

If your income is below ₹10 lakh, forming HUF may not be worth the complexity. But if you are earning well and building assets seriously — ignoring HUF is financially lazy.

Compliance Requirements

- Separate PAN

- Separate bank account

- Separate books (if business)

- Separate ITR filing

- Proper documentation of gifts

This is not “set and forget.” This is disciplined structuring.

HUF vs Individual Taxation: Quick Comparison

| Feature | Individual | HUF |

|---|---|---|

| Separate PAN | Yes | Yes |

| Basic exemption | Yes | Yes |

| 80C limit | ₹1.5L | ₹1.5L |

| Capital gains tax | Applicable | Applicable |

| Legal status | Person | Separate entity |

Think of HUF as adding one more tax-paying bucket for your family wealth. More buckets = more flexibility.

When Should You Consider HUF?

You should strongly consider it if: you are in 30% slab, have ancestral property, long-term equity investments, run a family business, want generational planning.

You should avoid it if: income is low, no family assets, you prefer simplicity over optimization.

Strategic Wealth Framework Using HUF

Step 1: Audit Your Income

Salary, capital gains, rental, business income.

Step 2: Identify Transferable Assets

Ancestral property? Gifts? Family capital pool?

Step 3: Estimate Tax Differential

Calculate tax if individual vs if HUF. If meaningful → proceed.

Step 4: Create HUF Properly

Draft deed, apply PAN, open bank account, document capital introduction.

Step 5: Invest Strategically

Create long-term equity corpus, rental asset base, dividend income layer. Make HUF a wealth engine.

Psychological Advantage Most People Ignore

When investments sit in HUF, they feel “family-owned.” That reduces impulsive selling, emotional decisions, improves long-term discipline. Structure creates behavior. Behavior builds wealth.

Final Thoughts: Use It Intelligently, Not Emotionally

HUF is not for everyone. But if used correctly, it is one of the most underutilized tax planning tools in India. Wealth is built by efficient taxation, structured ownership, legal optimization, long-term discipline.

One Question for You

Are you focusing more on chasing returns… or on structuring your wealth intelligently? Because the second one often matters more.

If you want, I can next help you create a HUF setup checklist or calculate potential tax savings for your situation. But be clear first: are you optimizing — or just reacting?

Entity to Save Taxes on Investments in India){kind=link}