Digital Rupee (CBDC) — Future of Money in India | Investor Guide

🇮🇳 Digital Rupee (CBDC): Future of Money in India? A Complete Investor & Trader Guide

⚡ Structural shift led by RBI | Central Bank Digital Currency — early-stage disruption

CBDC visual overview

State adoption pilots

RBI issued digital cash

Legal tender e₹

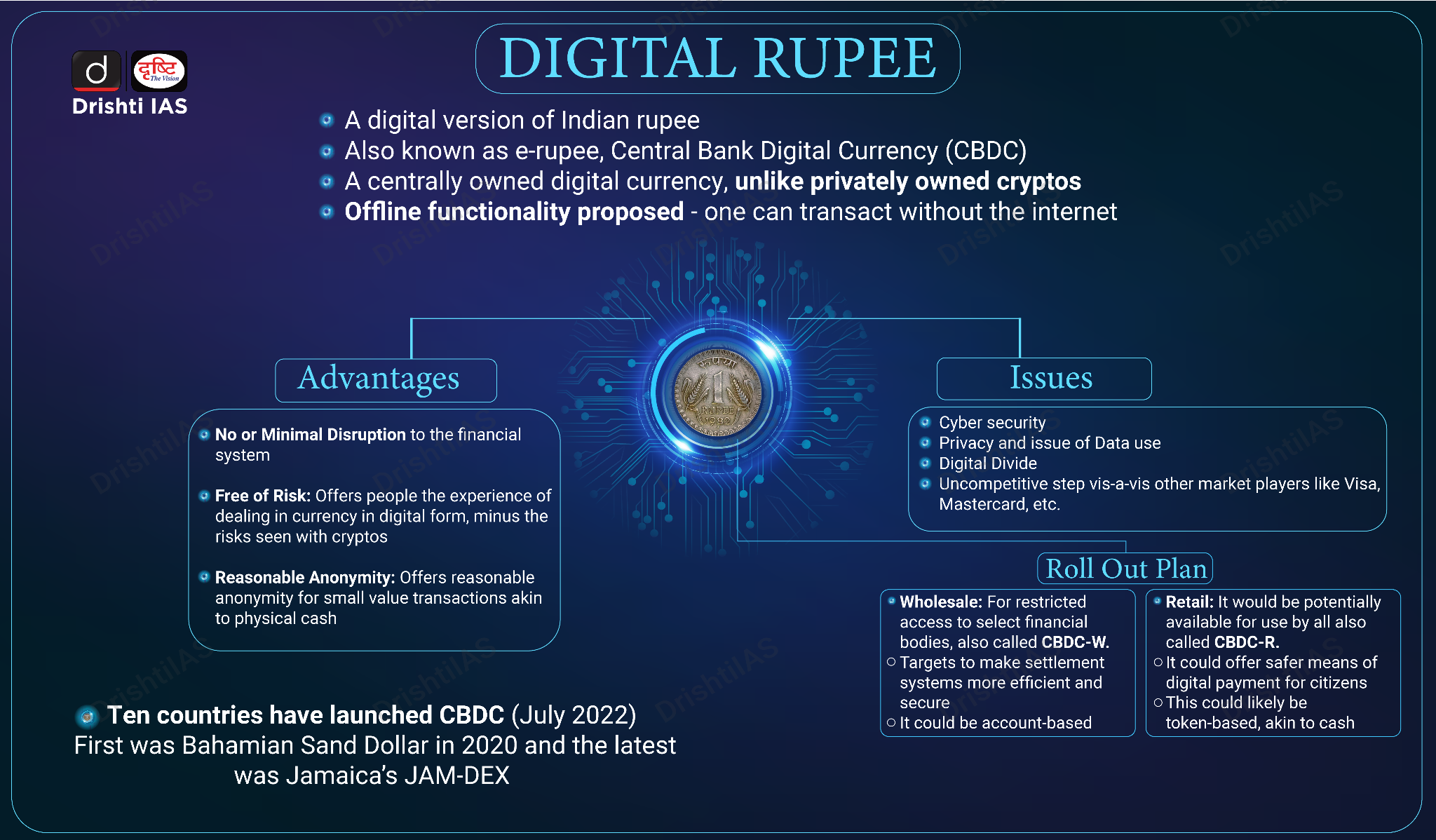

📊 What Is Digital Rupee (CBDC)?

The Digital Rupee (e₹) is a digital version of physical cash issued directly by RBI. Unlike UPI or wallets that rely on private intermediaries, the Digital Rupee is central bank money — legal tender just like banknotes. In simple terms: it's like holding cash, but in digital form.

🔹 Issued & backed by RBI Full sovereign guarantee, zero credit risk.

🔹 Legal tender (same as ₹ cash) Everyone must accept it for transactions.

🔹 Stored in digital wallets RBI-provided or partner apps.

🔹 Works without bank dependency Peer-to-peer, no intermediary required.

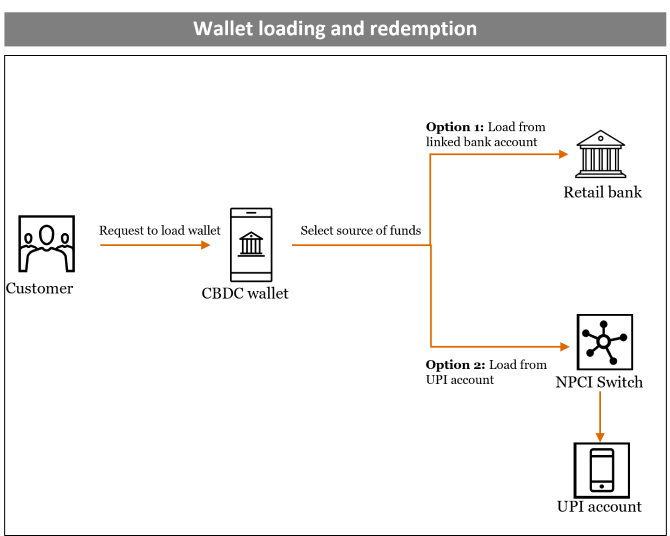

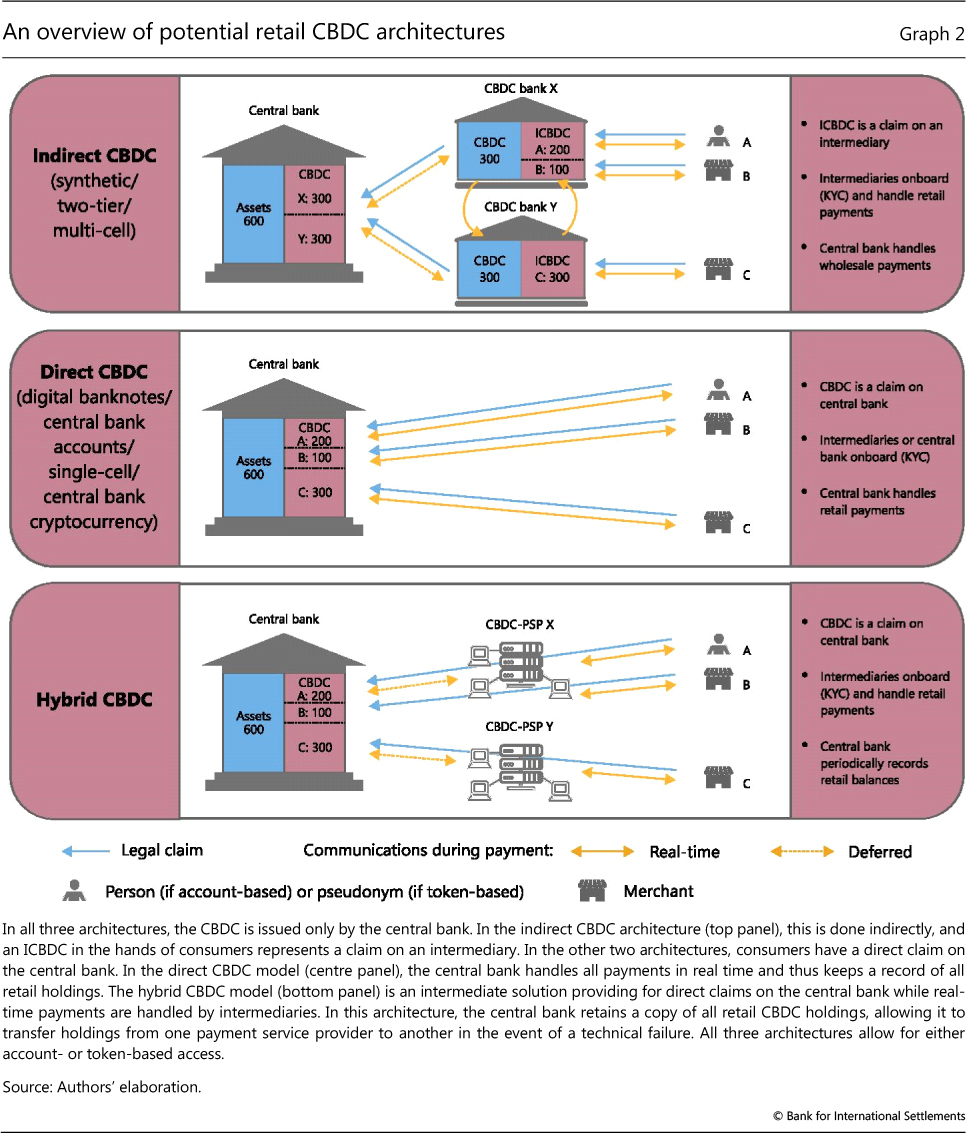

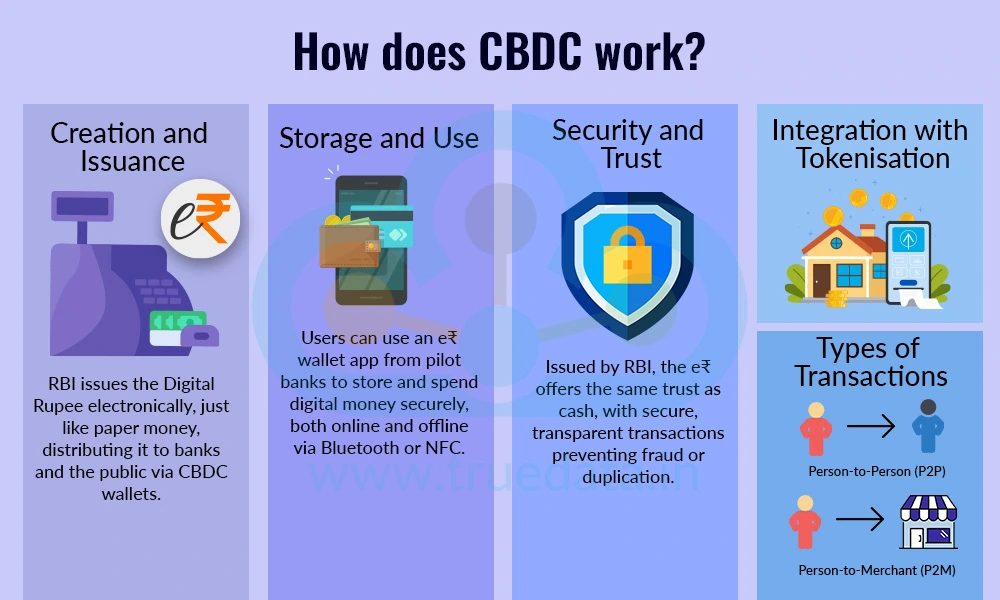

⚙️ How Digital Rupee Works

Retail & wholesale flows

Two-tier system (BIS)

Token based digital cash

RBI retail pilot

🔹 Retail CBDC (e₹-R) → For public use, works like digital cash, peer-to-peer transactions. 🔹 Wholesale CBDC (e₹-W) → For interbank settlements, improves efficiency in large-value transfers.

💡 Why RBI Is Launching Digital Rupee

🔥 1. Reduce Cash Dependency Lower cost of printing, transport, and counterfeiting risks.

🔐 2. Better Control Over Money Supply Real-time visibility & monetary policy effectiveness.

🌍 3. Compete with Cryptocurrencies Provide stable, government-backed alternative to volatile private crypto.

📈 4. Financial Inclusion Direct access to digital money for unbanked population.

⚔️ Digital Rupee vs UPI vs Crypto

CBDC vs crypto vs UPI

UPI moves money, CBDC is money

Global CBDC trends

Stable vs volatile

Parameter

Digital Rupee (CBDC)

UPI

Crypto (Bitcoin/Eth)

Issuer

RBI (Central Bank)

NPCI + Banks

Decentralized network

Legal status

Legal tender

Payment system

Not legal tender in India

Volatility

Stable (₹ pegged)

Stable (fiat transfer)

High volatility

Nature

Digital form of cash

Payment rails

Speculative asset

📉 Impact on Banking System

🏦 1. Reduced Role of Banks? People may hold RBI wallets → potential deposit outflows.

💸 2. Faster Transactions No intermediaries, instant settlement reduces friction.

⚠️ 3. Risk of Disintermediation Could disrupt traditional lending models if large deposit shifts occur.

📊 Impact on Stock Market & Traders

Market implications

RBI strategy

Fintech boom potential

Market expansion

🔥 Fintech Boom: CBDC adoption boosts innovation & new business models.

🏦 Banking Sector Pressure: Lower deposits & structural changes ahead.

📈 Market Transparency: Traceable digital money flow improves efficiency.

⚡ Faster Monetary Transmission: RBI policies reflect quickly in liquidity.

🧠 Hidden Insight (Most People Miss This)

CBDC is not just about payments — it’s about control + programmability of money. Future possibilities: targeted subsidies, conditional payments, real-time taxation. This changes how money behaves.

🚀 Challenges & Risks

⚠️ Privacy Concerns Transactions traceable; less anonymity vs cash.

⚠️ Cybersecurity Risks Digital systems prone to hacking threats.

⚠️ Banking Disruption Structural instability possible in transition.

📌 Is Digital Rupee the Future of Money in India?

Short answer: Yes — but gradually. Pilot phase (Now–3 years) limited adoption → Mid-term (3–7 years) wider integration → Long-term (10+ years) major monetary shift, reduced cash reliance.

🧩 Final Takeaway: Digital Rupee is a structural financial upgrade, a policy tool for RBI, and a signal of future systems. Understand it early → positioning advantage. Ignore it → react late.

🧠 One-Line Insight:“CBDC is not just digital money—it’s programmable economic power.”

?){kind=link}